The ebook market is growing faster as it grows larger.

The International Digital Publishing Forum (IDPF) on Friday reported U.S. wholesale ebook sales for January, 2010 were $31.9 million, up 261 percent from the same month a year earlier.

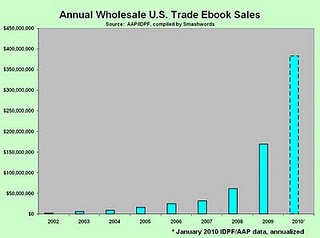

To put this in perspective, I created the chart at left. The chart compiles annual ebook sales data from the Association of American Publishers. For 2010, I took the latest IDPF January data and annualized it.

The data is collected from only 12-15 U.S. trade publishers. This means it dramatically understates what’s really happening in ebooks, because thousands of large and small publishers, as well as tens of thousands of independent authors, aren’t reporting their data. The data also doesn’t capture ebooks sold outside traditional retail channels.

The above omissions in no way invalidate the data, because as an indicator of direction and momentum, the AAP/IDPF data provides the best publicly available trending information I’m aware of.

What you see from my chart is that ebook sales grew nicely between 2002 and 2007, but were really too small to register on the radar screens of most industry watchers. Starting in 2008, however, the growth rate started to accelerate, and then this acceleration continued throughout 2009 and into the first month of 2010.

According to the AAP, in 2009 ebooks accounted for 3.31% of all trade book sales, up from only 1.19% in 2008. Even if sales stay flat from January onward in 2010, we’re looking at ebooks accounting for 6-8% of U.S. book sales in 2010. If sales accelerate further, a 10% monthly run rate is certainly likely by the end of this year. These numbers are dramatically higher than most reasonably-minded industry watchers predicted even a few months ago.

The rosy numbers above still dramatically underestimate the impact ebooks are having on the bottom line of authors, publishers and retailers. In January, during Amazon’s quarterly earnings conference call, Jeff Bezos announced that for books it sells in both Kindle and print formats, ebooks were then accounting for 60% of unit sales.

What’s driving the torrid growth of the U.S. ebook market?

Amazon deserves most of the credit. In January, Rory Maher of TBI Research reported that his publishing industry contacts were telling him that Amazon was accounting for 90% of all ebook sales. Other analysts have since confirmed those estimates.

The upcoming April 3 launch of Apple’s iPad, along with more aggressive moves by Google, Barnes & Noble, Sony and scores of other new ebook device makers and indie retailers, will no doubt try to chip away at Amazon’s purported 90% share.

The real story is not how or if these competitors take share from Amazon. It doesn’t matter. What matters is that an ever-growing pro-ebook crowd of powerful consumer-facing companies are pulling out all the stops to help spread the joy of ebooks to every corner of this book-hungry globe.

Why are consumers going ga ga over ebooks? Back in October, I blogged some of the reasons in my Huffington Post piece, Why Ebooks are Hot and Getting Hotter. I listed several reasons, such as the proliferation of exciting new e-reading devices; screen reading rivaling paper; content selection; free ebooks as the gateway drug; lower prices; and great selection.

If we boil it all down to what really matters, it’s about customer experience. People who try ebooks are loving ebooks.

Lest we think ebook reading is all about pricey jet set devices like the iPad, Kindle, Sony Reader and B&N nook, it’s worth considering some telling data that came out of the latest Book Industry Study Group survey. As I reported in my Tools of Change conference wrap-up, BISG found that 47% of all ebook reading is happening not on these new-fangled devices, but on ordinary computer screens.

Editor’s Note: The original posting can be found on the Smashwords blog. PB

Those reported percentages are Dollar amounts, not unit sales, right? Which means that, since Kindle ebook pricing tends to be lower than their competitors’, the unit sales percentage is likely a bit higher.

Still, even 90% is a lot. Absurdly high. (Unsustainably high under normal competitive conditions. But we’re no longer looking at normal competitive conditions thanks to the BPHs.) Especially since it doesn’t include Mobipocket sales at non-Amazon storefronts. Add-in DRM-free, Mobipocket, LRF, and LIT legacy DRM sales and it looks like the Adobe Adept ecosystem is running maybe, what? 5% of the market…? Surprising. So much for the annointed “industry standard”… No wonder Amazon ignores ePub.

On the hardware size, Kindle pricing is probably a tad higher than the competition so odds are that their unit sales are a bit less than the reported 69% market share. Say 60-66%? Makes the ebook to reader ratio 25-30% higher than expected if everything were equal, no? It is early in the game, but clearly Amazon *must* be cherry-picking the most active ebook buyers.

Once you factor in non-dedicated gadget readership, it should be pretty clear that, yes, the Amazon storefront is driving sales to Kindle, not Kindle to the storefront. While hardly a shock that has to be ominous news to the anything-but-amazon axis.

Retailers counting on hardware features and branding to drive volume may need to rethink their strategy. Fast.

So far, the “industry standard” ePub/ADE axis doesn’t seem to be moving much in the way of ebooks. Maybe that’s the real reason for the BPHs’ ill-considered price-fixing move and 30% price hike, to try to blunt Amazon’s pummeling of the alternate channels. Too bad their approach is more likely to cement Kindle’s domination. Because for the next year or two the bulk of their price-fixed ebooks are going to go to either Amazon (the installed base rules) or Apple (the sole beneficiary of the price-fix/price-hike).

The price-fix move may be targetted at Amazon but it is more likely to hurt Adobe’s infant ecosystem than it is to hurt Kindle because by reducing price-based competition, the BPHs are favoring walled-garden ecosystems (which can implement hardware-subsidized models) over open ecosystems. Which means Kindle and Apple and, maybe Skiff.

Of course, that assumes Apple’s iBookstore actually makes any kind of dent in the ebook market, which is no certainty. And if Apple does fall flat on its iPad, say by selling hardware but not eBooks, we may be looking at similar numbers this time next year.

An interesting comment to be sure. There are several other perspectives though.First this is USA only. In much of the rest of the world Amazon hardly figures, though admittedly neither do ebooks really. Secondly while there are ways and means to roughly estimate number of Kindles sold we have no ways of verifying the supposed 90% marketshare by Amazon of ebooks. Anonymous leaks to analysts surely cannot count?

(Given the supply problems Sony and B&N had during the last holiday season it is perhaps possible that during that specific period Amazon had 90% of all sales).

The estimates I’ve seen suggests a Kindle marketshare of ereaders somewhere between the low and high 60%. As you reasoned it is their storefront that attracts. Why? Mainly pricing and selection. Pricing will – theoretically – no longer be such an advantage. That leaves selection. There is only one company that could possibly equal or better that.

Google Editions has been so long in coming that skepticism is perhaps warranted, but if it arrives, supposedly mid-year, it will change things much more radically than the iPad. The flood of coming e-readers will finally have a partner and if Google is going to be a wholesaler as well then content will no longer be such a problem for the Adobe/epub bookstores.

(Also there is some reason to think that Amazon is converting their own customerbase towards ebooks. In one of the Forrester surveys Amazon buyers were much more interested in buying an ereader than Barnes & Noble patrons. It would be interesting to know how much cannibalizing of their own print readership has occured).

Finally I must comment on the idea of price based competition. Who exactly was going to beat Amazon at pricing?

eBook price competition?

Easy!

Other ebooks, of course.

In a free price-competitive marketplace, consumer purchasing decisions aren’t really about which store to buy from (Kindle owners only buy BPH books from Amazon, non-Kindle owners *can’t* buy from Amazon. Not legally, anyway.). Consumer prchase decisions are really about publisher versus publisher, catalog versus catalog, author vs author.

Lost in all the Amazon vs Apple angst is that the BPH’s price fixing scheme is about fixing prices across the board: all publishers, all authors. Mid-list authors priced the same as the popular “Name” authors.

Where, before, retailers could adjust the pricing of less-popular titles and authors to let them find an optimum sales rate (and we’ve all seen Amazon do just that with eBooks over the last two years), the price-fixing straightjacket will force consumers to pay the same price for a newcomer as for an established author. You know, the kind of author getting the big million-dollar advances and massive advertising campaigns from the BPHs? Yeah, that’s going to really help non-superstar authors, right?

The BPHs seem to think that Amazon is going to take their extra 25% profit margin and laugh all the way to the bank while their market share steadily erodes. And maybe they’re right. But they could just as easily be wrong; Amazon can also take their “forced windfall” profits and reinvest them to expand their presence in the ebook business. Maybe by going upstream and doing more publishing themselves. Maybe by buying up some mid-range publishers. Or maybe they’ll move downstream and expand their presence in ebook readers and tablets by subsidizing hardware prices, especially in the international markets they’ve only just started to address.

Amazon is a big, lean, creative company to start with. Does anybody really think that giving them an extra 25% profit margin to be creative with is going to be anything but bad for competition?

So we’re looking at a near term market divided between Kindle, Apple (assuming the Apple faithful show up in typical droves), and the small-fry huddling around the Adobe Adept “standard”. Now throw Google into the mix. They’ve shown they’re not afraid to do hardware and they are preparing to go to war with apple (and vice-versa) so a Google-Pad and/or Google reader are inevitable.

The market may be exploding buts its not exploding fast enough to satisfy all those monsters. And Amazon is not going down easy or soon. So odds are its the other wannabe players that are going to be squeezed out first.

Absent the ability to compete at the storefront level the only way left to compete is either through platform-exclusive content or through hardware pricing. Anyway you slice it, the near term ebook industry is going to start to look a lot like the gaming console business thanks to the price-fixing gambit.

Nothing good will come of this.

You make a strong argument – but I’m unconvinced. You seem to concede my point by noting that the real price differentiation was between author ‘brands’ and not storefronts. That is exactly my point – no ebookstore was beating – or going to beat – Amazon at pricing.

Being in retail myself I find that consumers do in fact look carefully at same goods pricing between stores. In the USA Walmart is the perfect example of beating everyone else on pricing. Amazon is the (would be) internet Walmart. So we both seem to agree that price competition storewise is a chimera.

Your perspective on the proposed BPH pricing schema is interesting. I’ve not investigated the agency model in-depth myself and will try and rectify that asap. Publishers would have to be even more stupid than they appear to price brand name and no name the same. The agency model is anyway only starting in May with Macmillan, not sure that anybody else will be onboard by then.

Rumour has it that certain of the publishers have monthly contracts and I suspect they will try to retain those. Watch what happens with Macmillan and the agency model for 2 to 3 months, only sign short term contracts – that would be my strategy anyway.

I’m not sure where that 25% extra profits for Amazon is coming from. Perhaps you believe Amazon was making a loss on ebooks – http://www.munseys.com/technosnarl/?p=913 does not believe it, neither does http://www.tobiasbuckell.com/2010/02/05/why-do-people-want-more-expensive-backlist-books/ , and you can count me with the skeptics. Of course on the big $9.99 bestsellers its loss will now be transformed into a profit but their margins on everything else will likely suffer. That would explain their ferocious attempts to keep the status quo since the new model destroys their model without giving them significant margin to change strategy.

Your vision of a three way war between Apple, Amazon and Google is spot on, except that the small fry will huddle under Google’s bulk. Google will use epub and as I understand it also Adobe DRM. It will supply every ereader, bookstore and would be entrant with access to Google Editions. It is the only way that the now miserable epub ‘standard’ could possibly become a standard and Google will use that as its strategy to both try and overwhelm Amazon and smother the iPad in its crib. Of course I could be wrong but this is pretty much the very successful strategy it is following in the mobile business.

I believe this is all inevitable since these monsters want to control all of digital content – books, music, movies, you name it. We can, so to speak, make bets on the winner, collect the stats, and cheer for our favorite teams.Get the good seats while they’re still available.

The price fix is set at 30% higher, no?

I’m granting the anti-amazon crowd a 5% cushion.

If amazon is actualy making a profit with variable pricing then the “windfall” is bigger, no?

And my point of price competition is that there is no meaningful price competition *after* an ecosystem is chosen. Price competition is very real *before* the customer commits to Kindle or Adobe. A lot of people have been choosing Kindle because Amazon prices average 15% or so less. Once they sign on to Kindle that no longer makes much of a difference.

With the new price-fixing regime, the Amazon storefront can *still* compete on price to the extent that it can retain pricing flexibility on small and medium publishers, which they could subsidize off their BPH “windfall”. So the scheme may actually buy the BPHs the worst of all worlds; kill the adobe epub competitors, hurt their own catalog, and strengthen Amazon’s competitive position. A bad idea all around.

Finally, if I was “small fry” I wouldn’t want my fate to depend on Google. But maybe that’s just me… 😉

I write scifi flash fiction and decided to put it into ebook form and posted it at my ebook where it has been read over a thousand times….perhaps I should sell it. I am trying to sell my newest novel Birthing the Lucifer star and I had some success but I need publicity, I’m new to the author game but I hope people stop in to read my new release http://publishitorbust.blogspot.com/ and leave comments or better yet a book review.

Nope, afraid I still don’t get it. As I understand it Amazon was getting discount of at least 50% on all ebooks. Some of these – the big bestsellers – were sold at below cost by Amazon so incurring a loss on those specific titles. On everything else they would be making a healthy margin. Now they would not be allowed any loss leaders. However the discount they get now is only 30%.

Difficult to say whether they are doing better or worse, since I don’t know what % of total sales the loss leaders were. If I had to guess the extra 20% they have lost across the board will not be made up by the profits now coming from the bestsellers. This is all speculation though as I’ve not seen any firm data. Amazon’s actions does not suggest to me that they think they are getting a better deal…but who knows? It could all be a double bluff.

I’m skeptical that Amazon will be able to hold on to small and medium publishers – it would be most unwise to sign long term contracts now.

Small fry have a simple choice – sign up with one of the big guys unless you want to be roadkill. Apple will not have them, Amazon could have gone this route but it’s probably too late. That leaves Google, them being for ‘free’ and all. If Google wins expect zero priced books but lots of ads in them. A bazillion!

Amazon gets a discount of 30% of an enforced price of $13 dollars, where before they got an unspecified profit (or suspected loss) at $10. Regardless of what they were previously clearing, they will now clear an extra 30% of price-fixed books.

The fun part is figuring out how Amazon can use that extra cash-flow to increase their market power.

Lots of ideas come to mind.

Don’t forget that Amazon is actually quite large with many subsidiaries and their real agenda may actually be quite complex in the long term.

http://newteleread.com/wordpress/2009/08/05/amazon-money-trail-helps-reveals-its-digital-strategy/

There is also a useful US market chart comparing percent print to screen over the last ten years. It is also set in dollars. This is at http://www.publishers.org/main/PressCenter/Archicves/2010_February/SalesUp4.1in2009Release.htm

It is notable that screen book growth begins and makes its climb to 3 % during a period of print growth. Another factor going forward is allocation of genres to screen or print format. Print can and has shed genres that were ill suited to the format. Screen may adopt some not yet represented. In any case these two trade sales measures should be watched together.

I think we might be talking apples and oranges here. I agree with everything you say up to a point. Amazon will now make a profit on its previous loss leaders.

However it was making a healthy margin (50% plus) on most of everything else. That margin will now shrink to 30%. Has anyone actually crunched the figures to see if the gains outweigh losses? Amazon only profits more if the loss leaders was a large percentage of their ebook sales previously – I’m not sure that’s the case. If Amazon’s actions and industry rumours are correct then they certainly don’t seem to believe they have gained anything.

We seem do be dealing with a known unknown here. Has anybody got actual hard data? Or perhaps I’m just missing something?

@Gous: Yes, we are talking different things.

In the retail model, Amazon *paid* 50% of the list price and sold the book for whatever they chose to. That is *not* the same as saying they had a 50% margin. Their margin was their sale price minus the 50% (minus whatever it cost them to sell the book; overhead, etc).

If Amazon had a 50% margin to work with, they would be selling the ebook at list price.

In the price-fix model, all books sell for $13 and Amazon has a fixed 30% cut (minus selling costs, as before). This is a forced increase in price to customers and in many cases a *cut* in the publisher (and author’s) take. Why would the BPHs force a model that results in lower ebook revenues? Reduced competition, more control, thinking higher ebook prices wil resultt in more print sales, thinking fixed prices will increased sale of “flagship” titles they granted massive advances to, lots of reasons, really…

Remember, the price-fix idea came from Apple because they wanted *fatter* margins than the old model provided. So rest assured, Amazon *will* have more money to play with (at consumer expense, of course) under the new model.

Which is why it is becoming so important to them to keep the fixed-price regime from spreading beyond the 5 BPHs drinking the Apple kool-aid.

Those 5 houses, for all their visibility, still reportedly control something less than half Amazon ebook sales. If their fixed-price regime helps Amazon turn the rest of their sales into “loss leaders” (through “basket pricing”) then the Amazon storefront would *still* be *on average* cheaper than competing storefronts. Which makes the Kindle walled-garden preferable to its competitors. The details change but the landscape remains the same: that’s why I originally said we might be looking at similar sales share numbers a year from now. Walled garden platforms all share a network effects “halo” that makes the installed base crucial because the walled garden lock-in ensures that present platform customers are more likely to remain customers in the future.

Depending on how aggressive they want to be, Amazon could end up, in effect, subsidizing small and mid-size publishers who stick with the retail model, using BPH money. At a minimum, they could wield the power of “temporary sales” to drive short-term revenue boosts to books and publishers they favor. That is a seriously useful power and it is even more useful if the BPHs prices are fixed but their smaller competitors’ prices remain flexible.

The only way the cartel’s fixed-price scheme actually hurts Amazon is if *every* publisher insists on pricefixing their books.

That’s a big if.